SMM reported on July 10:

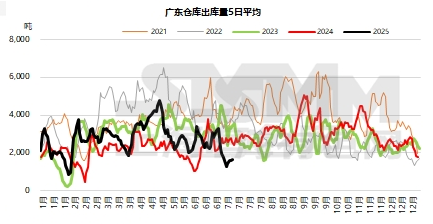

Guangdong region: This week, premiums and discounts in the region continued to decline. Despite a significant pullback in copper prices, consumption recovery remained slow. Coupled with an increase in arrivals, spot inventory rose for nine consecutive weeks, leading to a decline in premiums under pressure. As of Thursday, high-quality copper was quoted at a premium of 50 yuan/mt, down 50 yuan/mt from last Thursday. Standard-quality copper was quoted at a discount of 100 yuan/mt, down 130 yuan/mt from last Thursday. SX-EW copper was quoted at a discount of 150 yuan/mt, down 130 yuan/mt from last Thursday. On Thursday, the price spread between Shanghai and Guangdong for standard-quality copper premiums and discounts was 70 yuan/mt higher in Shanghai, with a relatively small spread, leaving no room for cross-regional cargo transfers. According to SMM statistics, as of Thursday, the total inventory in Guangdong warehouses was 23,900 mt, an increase of 5,200 mt from last Thursday. The total warrants were 9,500 mt, an increase of 3,200 mt from last Thursday. With relatively large spot discounts, suppliers chose to transfer cargoes to warehouses, leading to an increase in warrants. Specifically: This week, warehouse arrivals were 13,200 mt/week, an increase of 4,000 mt/week from last week, slightly below the annual average (14,000 mt/week). Weak consumption led suppliers to transfer cargoes to warehouses. Outflows from warehouses were 8,300 mt/week, a slight increase of 2,000 mt/week from last week, far below the annual average (14,200 mt/week). Although copper prices declined, downstream consumption recovery remained slow, resulting in relatively little change in shipments.

Looking ahead to next week, we understand that imported copper arrivals will be limited, but domestic copper arrivals will increase. However, after copper prices continue to decline, downstream procurement volume is expected to increase compared to this week. Therefore, we believe that next week will see an increase in both supply and demand, with weekly inventory expected to decline again and premiums rebounding.

》Subscribe to view SMM metal spot historical prices

(The above information is based on market collection and comprehensive assessment by the SMM research team. The information provided is for reference only. This article does not constitute direct advice for investment research decisions. Clients should make cautious decisions and not rely on this as a substitute for independent judgment. Any decisions made by clients are unrelated to SMM.)